Tokens: not just for the subway anymore

The word token is thrown around liberally these days, though it had a history long before blockchain. Physical tokens have been around for millennia. So what is it about blockchain-based tokens that sets them apart from their predecessors?

Not all that much, it turns out.

This short piece is a point-in-time mapping of what blockchain-based tokens are out there today, how they relate to each other, and which ones you might run into in real life.

1. What is a token, exactly?

In the 1970s, a token was a piece of metal or paper that got you a ride on the subway. In technical terms, that token represented a claim on the services of the subway company to transport its holder from one location to another.

In the same way, blockchain-powered tokens such as stablecoins are defined by their representation of value. In their taxonomy of cryptographic assets, the Global Digital Finance association defines tokens as: “legal instantiations of a share of an asset, a set of permissions, or a set of claims that are held by the bearer(s) of said token.”

There are two important parts to this definition: (1) A token is a representation of value, and (2) The value of the token is conferred to the bearer (holder) of the token.

Together these two features define the universe of digital, blockchain-based tokens. These include, but are not restricted to: Central Bank Digital Currencies (CBDCs), stablecoins, intra-bank tokens, security tokens, cryptocurrencies and NFTs. Now that we know what they all have in common, let’s discuss what differentiates them.

2. Here’s how you can distinguish between different types of tokens

If someone asked you to tell them the difference between JPM Coin, USDT, and the Bahamas Sand Dollar, could you do it in two sentences? We couldn’t either.

The reason it’s so difficult to compare different types of tokens is because they don’t exist on a single spectrum. Rather, they can be classified in various ways. For simplicity, we settled on the four below:

- Wholesale vs retail: Is the token used mainly for wholesale or retail transactions?

- Fungible vs non-fungible: Can the token be substituted 1:1 for another one of its type?

- Regulated vs non-regulated: Is the issuer registered or associated with a domestic authority?

- Asset-backed vs non-asset-backed: Is the token redeemable for its underlying asset outside the DLT network?

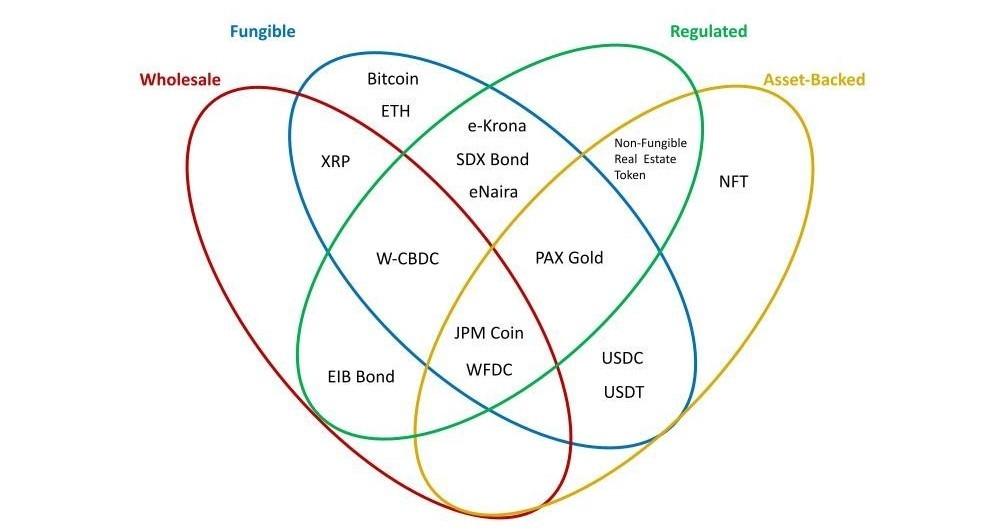

Figure 1 populates these categories with some commonly-used tokens. But first, three caveats. First, the categories we include are not yet settled. We have a whole section below on what “regulated” means. Second, no official token glossary exists (though there are ongoing efforts at both the platform level and the legislative level). And finally, we make some judgement calls about token types that technically fall into multiple categories. XRP falls into the wholesale category because even while XRP can be purchased by retail customers, only institutional customers can use RippleNet.

You might also notice that some things are missing from the figure. We don’t include utility coins because they represent a subset of cryptocurrencies. We also left out some prominent tokens if they don’t use blockchain for all use cases. One example here is China’s CBDC, called the DC/EP, which uses blockchain in a limited fashion.

Figure 1: Some different ways to categorize your tokens

- Stablecoins are represented by USDT, USDC

- Cryptocurrencies are represented by Bitcoin, XRP for RippleNet, and ETH

- CBDCS are represented by Sweden’s eKrona, Nigeria’s eNaira, and wholesale CBDC (wCBDC)

- Intra-bank tokens are represented by JPM Coin and Wells Fargo Digital Cash (WFDC)

- Security tokens are represented by SDX bond, PAX Gold, and the Non-fungible Real Estate Token

- Other tokens include the European Investment Bank’s EIB Bond, and Non-fungible Tokens (NFTs)

The figure mostly uses specific examples rather than general categories. This allows us to highlight the within-category variation that results from different design choices. For example, the category of CBDCs can be either retail such as the Bahamas Sand Dollar or wholesale CBDCs.

This variation is also apparent for security tokens. They can be classified as fungible or non-fungible, depending on the underlying asset that they represent (e.g. a security token representing a bond vs a security token representing a specific geographical/spatial fraction of a building). Security tokens can also be classified as asset-backed or non asset-backed. Based on our definition above, some security tokens may represent legal ownership of existing assets sitting with a custodian (hence redeemable, e.g. Paxos Gold), while others may be natively issued and recorded on the blockchain (e.g. SDX bond issuance).

This variation within categories reflects the magnitude of experimentation happening today as issuers try out different features. This is also highlighted by XRP and Bitcoin’s separate placements in the figure. Although both are cryptocurrencies, XRP was developed for wholesale transactions while Bitcoin was developed for retail transactions.

3. “Regulated” tokens aren’t what you think

In Figure 1, we include the category of regulated tokens even though most jurisdictions do not (yet) systematically regulate tokens. The tokens that fall into the regulated category are those which either represent regulated assets, such as security tokens or those which are issued by the regulator, like CBDCs.

The term “regulated” understates the complexity of what is going on. It is not the case that some tokens or token issuers are regulated and others are not. The IMF points out that most stablecoins fall into a category they call “partially regulated” which means that elements of the stablecoin arrangement are regulated. And no stablecoin falls into the category the IMF calls “comprehensively regulated.” For those tokens that are issued by regulators, like CBDCs, we can also expect that once cross-border use cases occur, additional regulations will be required.

The first token that falls into our “regulated” category is security tokens. Because they represent highly regulated securities, they are scrutinized by the SEC in the US, and its equivalents worldwide. A recent example of a successful security token issuance is SDX in Switzerland. There, the Swiss regulator was directly involved in the issuance of a digital bond, and has ensured SDX is registered as a licensed stock exchange and a Central Securities Depository (CSD).

A second entry into our “regulated” category is CBDCs. We defined them as regulated by virtue of their issuance by the central bank in a given jurisdiction. The wave of interest in CBDCs has accelerated as governments have become more cognizant of the benefits of digital tokenization. As the traditional controllers of sovereign currency, central banks are legally obligated to understand the implications of private sector money on the money supply and on financial stability. As part of the research, it has become clear that tokens might be adopted as a tool of monetary policy as well. There are a number of design choices that can be made, and lively discussions are continuing.

Stablecoins currently fall into a grey area, since some issuers are trying to appeal to risk averse investors by aligning parts of their business with existing regulations intended for other types of operators. Some issuers, such as Tether, remain almost entirely unregulated, though a more common strategy is for stablecoin issuers to align themselves to existing e-Money or cryptocurrency regulations. For example in the US, Circle (USDC) has a New York State BitLicense, is registered with FinCEN and has multi-state Money Transfer Operator licenses, while Paxos has a NY State BitLicense and a Federal Trust Charter with the OCC. They are different, but neither is more or less correct. Until there are more explicit licensing regimes, we can expect this situation to continue.

It is likely that new regulations will continue to come online to even out this space in coming years. In the US, the President’s Working Group on Financial Markets, joined by the FDIC and the OCC, recently released a paper calling for more systematic legislative regulation.

4. Stablecoins: the grey zone

Stablecoins are a class of crypto assets that gained popularity following the 2018 Bitcoin price crash. There is no legal definition yet, but many international standards bodies define this as a type of token designed to maintain price stability relative to some external assets (in contrast to cryptocurrency volatility).

The concept of financial tokens that represent other financial assets is not new. We’ve seen it since 1969 with the IMF’s special drawing rights (SDRs), for example, which are tied to a basket of currencies. But in the case of stablecoins, price stability is commonly achieved by pegging or tracking to some reference asset. This can be the US Dollar, as in USDP, or gold like Digix.

There are three primary uses of stablecoins today:

- The most common use at the moment is in cryptocurrency trading. Traders can more quickly realize gains from crypto volatility by converting it into a stablecoin. This can happen instantly rather than converting gains to a reserve currency which takes some time and incurs some risk.

- A second use of stablecoins is in cross-border payments. Examples of this are primarily in development and include Fnality USC and a Korean Won-backed stablecoin. While this use is less common, it has attracted sufficient attention that it has been added as an item in the FSB’s G20 roadmap and the US President’s Working Group report.

- A third way in which stablecoins are used today is for intra-network transactions. Tokens used in this way transfer value within a network between entities. Because the use case is closed-loop, these tokens are not available to retail users.

5. How are tokens impacting our day-to-day activities?

You and I engage with all of these types of tokens in different ways. For some readers, you’re holders of crypto or stablecoins. You’re investing, trading or using tokens to transfer value. For others, you might be a beneficiary of faster settlement if your bank is using tokens. If you live in a country with a retail CBDC, you might have access to a new payment instrument.

In the end, the existence of all of these new token types signals that there is ongoing innovation in payments, ownership, investment and governance. We’re starting to see some of this innovation in activities like the rise of DAOs as auction winners and multiple CBDC projects moving closer to production. Beyond being involved as a platform, R3’s Sandbox for Digital Currencies has been deployed as a tool to help understand the different design choices that are available.

This is just the beginning of this conversation. And these definitions will continue to change. We’d love your feedback on these definitions and issues. Email us to continue the conversation!

Definitions

- CBDC – a third version of central bank money (alongside cash and reserves) that could be used as a digital token to represent the digital form of a national currency.

- Cryptocurrency – a digital currency operating independently from a central bank and designed to work as a medium of exchange.

- Intra-bank tokens – a term that often describes a token issued by a bank for internal settlement, often backed by deposits. Sometimes called bank coins.

- NFT – represents a digitally unique asset. It cannot be broken down into smaller units.

- Security token – represents a real-world security, typically an economic stake in a legal entity. This means it is retail, fungible, fractionalized and programmable. Often, they pay interest and yield dividends.

- Stablecoin – token pegged to a stable reserve asset, designed to reduce volatility of cryptocurrencies.

- Utility token – tokens that provide value by granting holders access to a service or future product.